Yaar, hum sabne ek time pe socha tha ki “ek bada ghar hoga, terrace par chai, weekend par barbeque, shaadi me cousin room, sab kuch perfect.” Lekin ab planning stage se hi lagta hai ki ghar kharidna ek Mission Impossible jaise hai — bas music background me chal raha hai 🎶 “This time… it’s impossible”.

Aur sach me, aaj agar tum ₹12 lakh saal ka salary earn karte ho, to socho — kaunse area me 3BHK ki EMI ₹40–50k monthly chalegi aur baki paise se zindagi chalegi… 🤔 Mission impossible hai kya? Nahi, yeh toh uncharted territory hai! 🤪

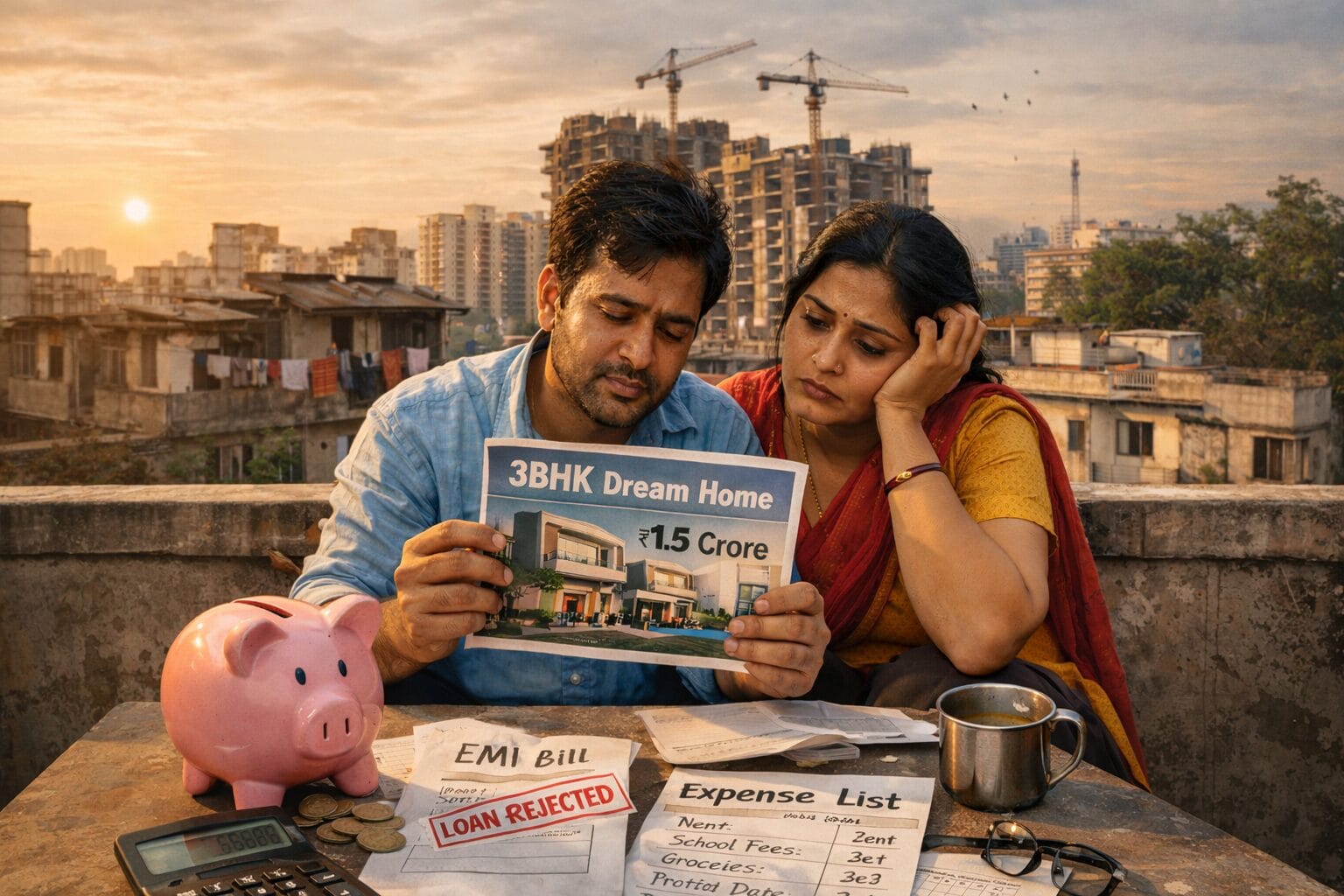

middle-class in india can never affrod a home but why ?

🏦 Reason #1: Salary Growth vs House Price Growth (Woh Dil Maange More!)

Pehle log sochte the ki salary badhti hai → house price bhi affordable hota jayega. Lol. Not in India. Reality:

🔹 Salaries India me modest pace se badh rahi hain — ~4–6% per year.

🔹 Property prices bohot fast grow kar rahe hain — ~9–11% per year (especially metros).

So simple math: Income vs Price = Tik-tik audio crescendo.

Matlab: tu jitna kama raha hai, usse zyada market tere sapne ko beat kar deta hai. 🥲

Jaise ek friend ne kaha:

“₹3,500 salary wali generation ne apni first house buy kiya 30 saal me… hum ₹27,000 pe bhi struggle kar rahe hain.” — jab inflation aur asset price growth ko adjust karein to salary ka purchasing power waise ka waise hai.

📈 Reason #2: Price-to-Income Ratio — Reality Check

Ek standard metric hai Price/Income Ratio, jo batata hai: ek house lene me kitne years ki salary chahiye.

Ideal worldwide benchmark ~5 hota hai. Lekin India me average ~11 hai. Meaning — sirf 1 house lene ke liye 11 saal ki salary! 😱

Aur kuch cities me:

- Mumbai MMR: 14.3

- Delhi: 10.1

- Kolkata: 5.8

- Chennai/Ahmedabad: ~5.1

… ye numbers middle class ka dream crush kar dete hain.

Soch, 30 saal ka career chal raha hai aur 11 saal sirf ek ghar pe ja raha hai, baaki zindagi ka kya?

💸 Reason #3: High EMI → The “Salary Vampire”

Banks happily de deti hain loan, bas condition hoti hai ki EMI ka 50–60% tera monthly income kha jaaye — wo bhi bina mercy ke. 😈

India ka average EMI/Income ratio ab ~61% hai — matlab zindagi ke bahut saare kharche sirf ghar ki EMI me chala jata hai.

Aur phir:

- Grocery bill

- Petrol prices

- Kids ki tuition

- Parents ka health checkup

Sab ke sab drama me, tumhare bank account se kha gaya ₹40,000 EMI … aur baaki ₹10,000 me “bread aur chai” ka combo pack chalana padta hai 😅.

also read : Why do Thinking beyond monthly salary is now become compulsory!

🏘️ Reason #4: Affordable Homes Disappear

Ab affordable housing — jo ₹40-50 lakh tak hoti thi — vo slow-slow vanish ho rahi hai. Builders ab luxury segment me zyada paise dekh rahe hain, jaha profit margin high hota hai.

2025 me affordable homes ka stock top cities me 30–60% tak gir gaya hai — Hyderabad me 70% tak kam hua, Mumbai me 60%.

Aur ek interesting fact?

2025 ki first half me 62% properties ₹1 crore+ me bik rahi the — matlab mid-class ke liye sasti options hi nahi bach rahi.

Toh simple baat:

Luxury properties jaldi bikti hain, budget wale ghar space me hi disappear ho gaye.

🪙 Reason #5: Hidden Taxes & Government Take

Bhai… property pe government bhi apna cut leti hai: stamp duty, registration, cess, infrastructure fees, land premium — in sab ka combo kabhi-kabhi property cost ka 30–50% tak ho jata hai! 😳

Simple analogy:

- House cost: ₹1 crore

- Government taxes, fees, approvals: ~₹30–50 lakh

- Final cost: ₹1.3 – ₹1.5 crore

Aur phir EMI bhi upar. Updated budget: Middle class ring me aa gaya out. 💥

🔁 Reason #6: Black Money + Corruption + Circle Rates

Real estate me jo “circle rate” hota hai — official value — usse log aksar lower dikhate hain 🧾, aur baki cash me settle karte hain. Isse transparency kam hoti hai aur market price artificially upar jata hai.

So real price me middle class buyers overpay karte hain, jabki black money wale investors market ko inflate kar dete hain.

🤹 Reason #7: Lifestyle Costs Bhi Upar

Aur bhai, ghar ke alawa bhi expenses hai life me:

- Petrol – vroom!

- College fees – kaise afford?

- Health emergencies – instant drama!

- Travel – once in a year dream.

In sab ne income growth aur expense growth ka gap aur badha diya.

Koh-i-noor wali growth kahaan hai? Naahi bhai, budget me inflation wali pinch hi milti hai. 😆

😅 Personal Experience (Just Like You & Me)

- Job start me: Salary decent thi, hopes high. 😎

- Search start kiya house ke liye: 2BHK saaf-sutri locality me ~₹60 lakh … socha “Chalo manageable.”

- Bank loan eligibility nikala: 😂 “Loan milega ₹40 lakh tak.”

- Down payment chahiye: ₹12 lakh.

→ Saving = ₹8 lakh.

→ Parents help = ₹4 lakh.

→ Wait = 2 years 🕐 - Price next year me ₹70 lakh ho gaya.

Moral of story: Income ne stagnate kiya, property ne level up kar liya. Reality hit harder than Netflix twist. 😩

🧠 Final Verdict: Middle Class vs House — Kaun Jeetega?

Short answer:

Aaj ka market middle class ko cushion nahi de raha. House prices salaries se fast grow karte hain, affordable homes kam ho rahe hain, taxes high hain, market incentives luxury ke taraf hain, aur everyday expenses ghar ka sapna tod dete hain.

Long answer:

Bina family support, inherited land, strong savings, aur strict financial discipline ke sath, house ownership still possible hai — par wo exception hai, rule nahi.

🎤 Conclusion :

Toh bhai log, agar tum soch rahe ho ki India me middle class kabhi ghar afford nahi kar payega, toh sach yeh hai — aaj ki date me ek typical salaried bandhu ke liye house dream jaisa ho gaya hai: optional luxury, not mainstream achievable goal! 😅

Way forward?

- Smart financial planning

- Second income ho toh best

- Tier-2/3 cities consider karo

- Aur budget loyalty mat todna

Kyuki EMI ki gulami se azaadi paana hai toh sirf paycheck aur dream equal nahi honge!

also read : How saving 10 lakh only can change your life forever in india

1 thought on “Why a middle-class in india can never affrod a home! reality in india!”