long story short

Table of Contents

Ghar banane ki baat ho aur dimaag me “The Engineer’s Choice” na aaye, aisa India me ho hi nahi sakta. Aaj ki date me UltraTech Cement sirf India ki No. 1 cement brand nahi hai, balki globally (China ko chhod kar) sales volume me No. 1 aur capacity me No. 2 ban chuki hai. Inki current capacity lagbhag 194 MTPA (Million Tonnes Per Annum) cross kar chuki hai.

Starting point: Aditya Birla Group ka Backbone

Pehle thoda background samajhte he. UltraTech actually Grasim Industries (Aditya Birla Group) ka cement division tha. 2004 me jab L&T ka cement business Aditya Birla Group ne acquire kiya, tab UltraTech officially ek alag listed entity ban gayi. Yeh ek masterstroke tha — ek hi deal me unhe massive manufacturing capacity, established distribution network, aur brand recognition mil gayi.

Socho isko aise: agar tum chess khel rahe ho, toh yeh ek move mein teen pieces advance karna tha.

Business Model ka Core: “Scale is Everything”

UltraTech ka poora business model ek simple lekin powerful idea pe built hai — jitna bada, utna better. Cement ek commodity business hai, matlab product me zyada differentiation nahi hota. Toh competition kahan hoti hai? Cost, distribution, aur brand trust me.

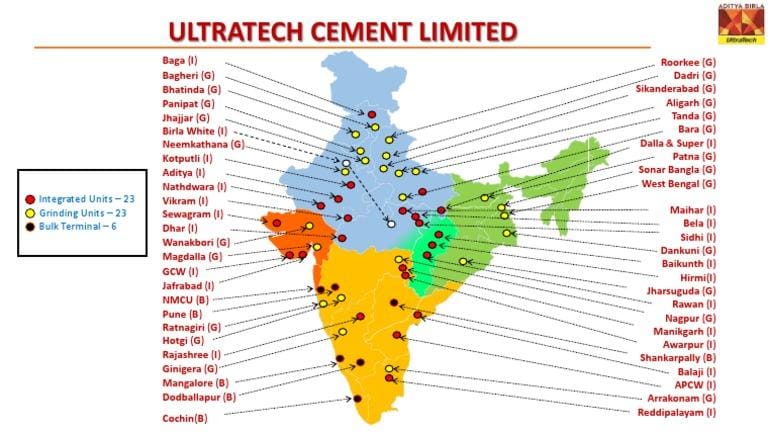

Manufacturing Scale: Aaj UltraTech ke paas India me 150+ million tonnes per annum (MTPA) ki installed capacity hai — yeh akele itna cement banate he jitna Pakistan aur Bangladesh milake banate ha. Jab aap itne bade scale pe produce karte ho, toh per unit cost dramatically girta hai. Isko economics me “economies of scale” kehte he.

Geographic Spread: UltraTech ne strategically apne plants raw material sources ke paas lagaye he — limestone mines ke close. Kyunki cement me raw material ka weight bahut zyada hota hai, transportation cost ek major expense hai. Plants ko mines ke paas rakhne se unka cost structure competitors se better rehta hai.

Distribution: The Real Moat

Ab yaha asli game hai. Cement ek aisa product hai jisko aap Amazon pe order nahi karte — yeh dealer network ke through bikta hai. UltraTech ne apna 50,000+ dealer/retailer network build kiya hai across India, including tier-2 aur tier-3 cities tak.

Isko aise samjho: ek contractor jab Rajasthan ke kisi chhote town me site pe cement mangata hai, toh woh pehle wahi brand maangega jo available ho, reliable ho, aur jiska naam usne suna ho. UltraTech ne yeh trifecta achieve kiya hai.

Unka “UltraTech Building Solutions” (UBS) stores concept bhi bahut smart hai — yeh basically ek one-stop shop hai jaha builder ko cement ke saath saath waterproofing, tile adhesive, ready-mix concrete sab milta hai. Is tarah unhone wallet share badhaaya — ek hi customer se zyada products ki sale.

Revenue Streams: Sirf Cement Nahi

Bahut log sochte hain UltraTech sirf bagged cement bechta hai. Actually unka model kaafi diversified hai:

Grey Cement (bulk of revenue) ke alawa unke paas White Cement hai — “Birla White” brand se, jo premium segment me market leader hai. White cement ki margins grey cement se kaafi zyada hoti he kyunki yeh finishing work me use hota hai.

Phir hai Ready Mix Concrete (RMC) — directly construction sites pe deliver kiya jaata hai. Yeh B2B segment hai jaha large real estate developers, infrastructure companies, aur government projects unke customers he. RMC me relationship-based selling hoti hai, isliye ek baar relationship ban jaaye toh sticky revenue milti hai.

Inorganic Growth: Acquisition Machine

UltraTech ki sabse badi strength yeh hai ki unhone India ka best acquisition playbook banaya hai cement sector me. Har baar jab koi smaller cement company struggle karti, ya koi conglomerate apna cement business sell karna chahta, UltraTech waha pahunch jaata tha:

2016 — Jaypee Cement ka acquisition: Jaiprakash Associates debt me doobi thi, UltraTech ne unke plants uthaa liye. 2017 — Binani Cement: IBC (Insolvency process) ke through. 2022 — Sanghi Cement (Gujarat): Coastal location ki wajah se strategic advantage.

Har acquisition ke saath ek pattern dikhta hai — UltraTech zyada operational efficiency laata hai, cost structure fix karta hai, aur apne brand + distribution me integrate kar deta hai. Yeh sirf buying nahi, transforming hai.

Sustainability aur Future Bet: “Green Cement”

Ab yahan UltraTech ki long-term thinking dikhti hai. Construction industry globally ek massive carbon emitter hai — cement production me CO₂ bahut nikalta hai. Government regulations aur ESG-conscious investors ki demand se chalta he, UltraTech ne “Net Zero by 2050” ka target set kiya hai.

Practically iska matlab hai ki woh blended cement (jisme slag aur fly ash use hota hai, jo byproducts he) zyada bana rahe he, green hydrogen experiments kar rahe he plants me, aur solar + wind energy se apni power needs meet karne ki koshish kar rahe he.

Yeh sirf PR nahi hai — iska direct business benefit hai. Jaise-jaise carbon taxes aur regulations tight honge, jo company pehle se green ho gayi hogi, uska cost advantage aur brand premium badhega. UltraTech yeh soch ke kuch saal pehle se invest kar rahi hai.

Brand Building: “Reliability” ka Psychology

Cement me brand building interesting hai. Consumer directly cement nahi kharidta — contractor ya mason kharidte he. Toh UltraTech ne apna marketing influencer model real life me apply kiya — contractors, civil engineers, aur architects ko educate karo, unhe loyal banao.

Unka “UltraTech Technical Cell” program yahi kaam karta hai — free training, site visits, technical support. Ek mason jo UltraTech ke saath comfortable ho gaya, woh apne next 100 projects me UltraTech hi specify karega. Yeh B2B relationship marketing ka best example hai India me.

The Numbers that Tell the Story

Aaj UltraTech ka market share India me roughly 22-23% hai — number 2 se almost double. Inki consolidated capacity globally bhi top 3 me aati hai (India, UAE, Bahrain, Sri Lanka, Bangladesh mein operations he). Revenue approximately ₹65,000+ crore annually hai.

UltraTech genuinely India ka No.1 cement brand hai — lekin iska matlab yeh nahi ki sab kuch perfect hai.

🔴 1. Commodity Trap: Differentiation Bahut Limited Hai

Yeh sabse fundamental problem hai. Cement ek pure commodity hai. Matlab — ek average consumer ya ek average contractor ke liye UltraTech ka OPC 53-grade cement aur Ambuja ka OPC 53-grade cement me koi measurable quality difference nahi hota. Dono ek hi IS standard follow karte he.

Iska practical implication yeh hai ki pricing power bahut limited hai. Agar UltraTech apna bag price zyada badhaye, dealer simply competitor ka bag recommend karna shuru kar deta hai. Isliye unhe hamesha ek uncomfortable balance maintain karna padta hai — naa itna sasta ki margin destroy ho, naa itna mahanga ki volume gir jaaye. Yeh tightrope walking constantly chalti rehti hai, aur recession ya slowdown me yeh rope aur bhi patli ho jaati hai.

🔴 2. Debt ka Bojh: Acquisitions ka Dark Side

Humne pehle UltraTech ki acquisition machine ki tarif ki thi — lekin usi machine ka ek dangerous side effect hai. Har acquisition debt ke saath aati hai. Jaypee, Binani, Sanghi — yeh sab deals amazing thi strategically, lekin inhe fund karne ke liye UltraTech ne significant borrowings liye.

Peak debt levels ₹25,000–30,000 crore ke aas paas gayi thi at various points. Ab debt reduction ho rahi hai, lekin interest burden ek structural cost ban jaata hai jo har quarter earnings ko eat karta hai. Agar cement demand slow ho — jaise COVID ke waqt hua — toh revenue girta hai lekin debt ka interest wahi rehta hai. Yeh operating leverage ka dark side hai.

Ek mental model yaad rakho: leverage ek amplifier hai. Jab cheezein achhi hoti hain, returns amplify hote hain. Jab buri hoti hain, losses bhi amplify hote hain.

🔴 3. Energy Cost Vulnerability: Inke Control Me Nahi

Cement banana ek extremely energy-intensive process hai. Limestone ko kiln me 1400–1500°C pe heat karna padta hai. UltraTech apni energy needs ke liye primarily coal aur petcoke pe dependent hai, aur yeh dono international commodity markets se price-linked he.

2022 me jab Russia-Ukraine war ke baad global coal prices spike kiye, UltraTech ke margins dramatically compress ho gaye — ek quarter me EBITDA margin 24–25% se girlke 17–18% tak aa gayi. Unhone kuch cost pass-on kiya, lekin saara nahi kar sake competition ki wajah se.

Yeh ek structural vulnerability hai jo company ke control ke baahir hai. Woh captive power plants banate he, solar lagaate he — sab achha hai — lekin complete energy independence abhi bahut door hai. Toh globally jab bhi geopolitical tension hoti hai, UltraTech ki P&L pe directly aasar padta hai.

🔴 4. Cyclical Business: India ki Economy ke Saath Bandha Hai

Cement demand directly real estate aur infrastructure spending se tied hai. Yeh dono inherently cyclical he. Jab government infrastructure spend karta hai aur real estate boom hota hai — UltraTech flies. Lekin jab:

Real estate me slowdown aata hai (jaise 2018–2020 ke beech IL&FS crisis ke baad), ya government capex slow ho jaata hai, ya interest rates badh jaate he aur home loans expensive ho jaate he — tab cement ki demand seedha impact hoti hai.

Is cyclicality ka matlab hai ki UltraTech ki earnings bahut predictable nahi he. Ek analyst ke liye yeh headache hai, ek long-term investor ke liye yeh risk hai. Company khud is cycle se bahar nahi nikal sakti — yeh business ki nature hai.

🔴 5. Competition Intensifying: Adani Factor

Ek naya aur increasingly serious threat hai — Adani Cement, jo ab Ambuja + ACC ke combination ke baad India ka No.2 player ban gaya hai. Aur Adani Group ki koi bhi company jo kisi market me enter karti hai, woh typically aggressive pricing, rapid capacity expansion, aur deep pockets laati hai.

Pehle UltraTech ek dominant No.1 tha aur baki sab fragmented competitors the. Ab for the first time ek well-capitalized, well-managed second player khada ho gaya hai jo seriously challenge kar sakta hai. Yeh consolidation from both sides hai — aur market share wars me ultimately margins suffer karti he — dono companies ki.

🔴 6. Overcapacity Risk: Supply > Demand

Cement industry me ek classic problem hai — everyone builds capacity at the same time. Jab demand outlook achha hota hai, sabhi players simultaneously capacity expansion announce karte he. Par plant build hone me 2–3 saal lagte he. Jab tak naye plants ready hote he, demand forecast galat bhi ho sakti hai.

India me aaj cement industry broadly overcapacity ki situation me hai — utilization levels 65–70% ke aas paas he, jo ideal 85–90% se kaafi kam hai. UltraTech bhi is industry-wide problem se alag nahi hai. Jab utilization low hota hai, pricing power aur bhi weak ho jaati hai.

🔴 7. ESG aur Carbon Transition: Upcoming Cost Burden

Humne pehle UltraTech ki green initiatives ki tarif ki thi. Lekin ek honest assessment yeh bhi hai ki net zero journey bahut expensive hogi. Carbon capture technology, green hydrogen, kiln replacement — yeh sab billions of dollars ki investments maangti hain jo abhi commercially proven bhi nahi he at scale.

Agar globally carbon border taxes implement hote he, ya India me carbon pricing aata hai, toh cement industry ko ek massive cost shock face karna padega. UltraTech ahead of curve hai, lekin “ahead of curve” ka matlab “immune to the curve” nahi hota.

Sab Milaakar: conclusion

Dekho, yeh sab bad signals he iska matlab ye nahi he ki UltraTech ek buri company hai — woh clearly nahi hai. Lekin ek informed person — chahe investor ho, business student ho, ya simply curious ho — ke liye yeh samajhna zaroori hai ki:

Moat real hai, lekin limitless nahi hai. Scale advantage meaningful hai, lekin commodity nature, energy dependence, debt legacy, aur now a serious competitor in Adani — yeh sab milke ek picture banate he jo sirf “India No.1 hai toh sab theek hai” se kaafi zyada complex hai.

Koi bhi business model permanent nahi hota. UltraTech ne past me jo challenges face kiye, unme se har ek ne unhe kuch naya seekhne pe majboor kiya. Future challenges bhi aise hi honge — aur yeh dekhna interesting rahega ki woh kaise respond karte hain. 🎯